Disadvantages of Adjustable Rate Mortgages

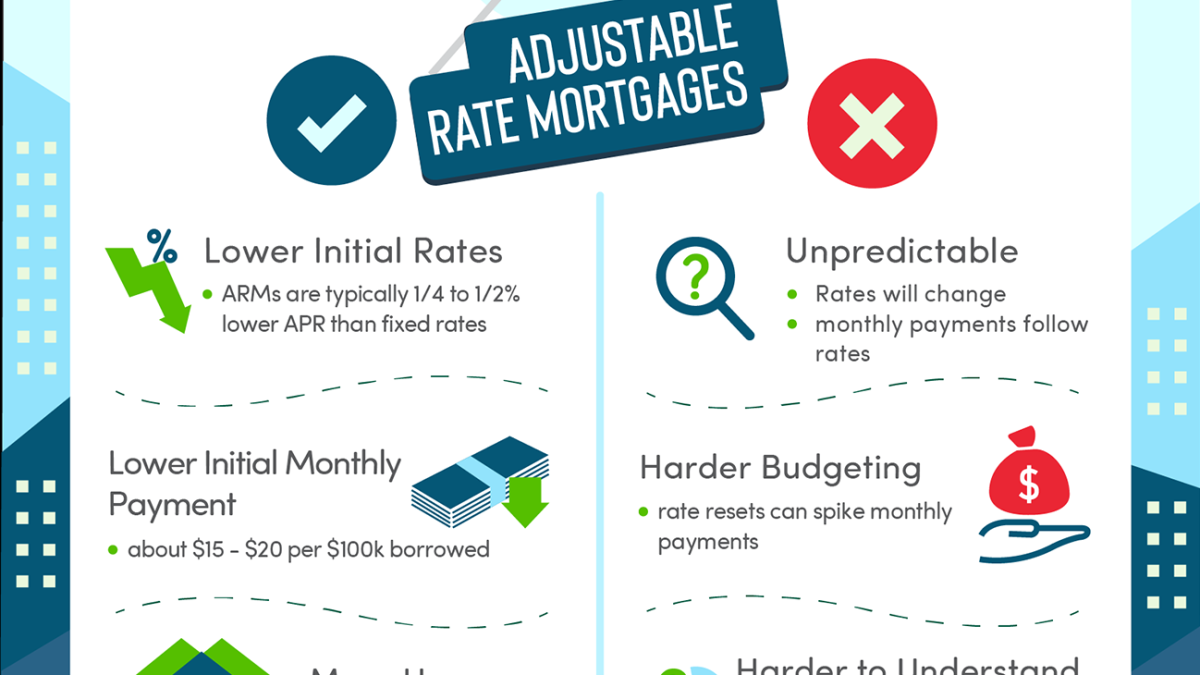

Whether you’re buying your first home, investing in real estate, or refinancing, an adjustable rate mortgage (ARM) is one option. This type of mortgage allows the borrower to set an initial interest rate and lock in the rate for a period of time, such as three, five, or ten years. The interest rate can then adjust periodically based on market rates. The initial interest rate is usually lower than a fixed rate mortgage, and it’s a good deal for consumers looking to get into a new home. However, adjustable rate mortgages come with disadvantages.

The biggest problem with an adjustable rate mortgage is that they come with prepayment penalties. In some cases, you’ll be charged thousands of dollars for refinancing to a fixed-rate mortgage, or to pay off the loan early.

Another disadvantage is the lack of flexibility. Depending on the lender, you may not be able to change your interest rate, change your payment, or even refinance to another ARM. In other cases, you may be locked into the highest rate possible. This can result in negative amortization, which is when you pay more than you owe. However, you can sell your home before the interest rate adjusts, or you can pay off the mortgage entirely.

Adjustable rate mortgages may have caps that limit the rate increase. This cap may be a 5% or 6% cap on the initial rate. It may also be a 2% cap on subsequent adjustments. These caps can be very complex. Some caps even limit the maximum monthly payment in absolute terms. The Federal Home Loan Bank Board has put together a mortgage checklist to help consumers understand their options.

The key to an adjustable life insurance policy is to pay off the loan in a timely manner. A good rule of thumb is that you can expect to pay more interest over the life of the loan than you would with a term life insurance policy.

Flexible premium adjustable life insurance is a popular option today. The policy is similar to universal life insurance, but allows the policyholder to adjust the death benefit, premiums, and other features of the policy to meet changing needs. The policy also has a cash value that grows as interest rates rise. This cash value can be used to pay premiums or to borrow against in the future. Flexible premium adjustable life insurance is popular because it allows the policyholder to plan for their future needs.

There are many other advantages and disadvantages to an adjustable rate mortgage, so it’s important to understand each one before you decide on the best option for you. You’ll be best served by determining your home use over the next five years, and determining whether an adjustable rate mortgage is right for you.

An adjustable life insurance policy will also come with an illustration that shows the current interest rate, the minimum interest rate, and the largest possible payment. You can also check out the annual statement, but be sure to look for the right information.